What does war risk insurance shipping actually cover?

War risk insurance shipping is not a niche add-on; it is the gating mechanism that keeps vessels commercially financeable when routes pass through conflict-adjacent waters. In standard marine programs, hull and machinery cover typically excludes war perils, which means owners need dedicated war clauses to cover losses tied to hostile acts, mines, missile strikes, detention, sabotage, or politically motivated seizure. Without that layer, a single strike can turn from an insured operational loss into a balance-sheet event that breaches debt covenants and counterparty requirements.

Coverage structure matters because the term "war risk" is often used as if it were one product. In practice, operators stack different elements: hull war cover for physical vessel loss, P&I war extensions for third-party liabilities, cargo war cover for goods in transit, and sometimes kidnap-and-ransom related protection for high-threat zones. Each layer has different triggers, exclusions, and notice obligations. A broker summary can sound broad, but settlement depends on exact wording in the placed policy and endorsements for listed areas.

The listing process itself is central. Underwriting committees frequently rely on defined "listed" or "high-risk" geographies and then quote additional premiums by transit. If your vessel enters a listed area without proper declaration, coverage can be impaired. That is why risk teams spend so much time on voyage declarations, notice periods, and accurate ETA/route statements. Administrative slippage can become a claims problem later, even if the physical incident is clearly conflict-linked.

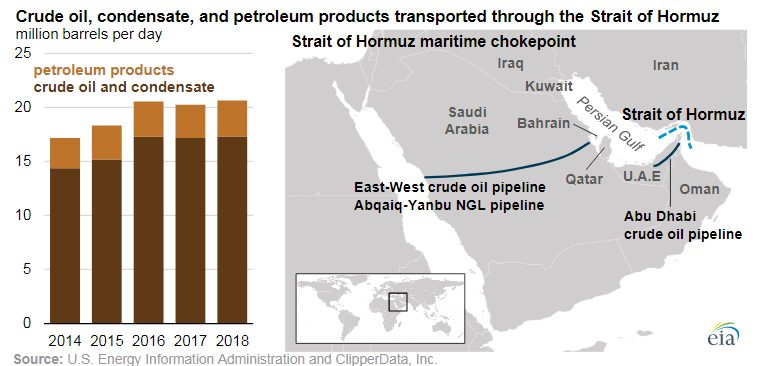

In the Gulf context, this is not abstract. The US Energy Information Administration's Strait of Hormuz chokepoint analysis shows how much global oil and LNG flow through the corridor. When that throughput is concentrated in a narrow lane, insurance markets react quickly to even limited attack activity because expected severity per incident is high. The premium signal can move before physical closures happen, and that cost change is often the first market indicator of perceived escalation risk.

Typical war-related triggers and exclusions

Most operators treat these as the minimum review list before fixing a voyage: hostile-action definition, terrorism wording, detention triggers, exclusion of nuclear contamination, sanctions compliance wording, and cancellation rights. A frequent source of confusion is the boundary between piracy-type exposure and war-type exposure; depending on jurisdiction and clause set, classification affects deductibles, notification, and whether the claim is even lodged under the expected policy. Sophisticated risk teams run clause-mapping exercises before an escalation cycle, not during it.

| Coverage element | What it can include | Common friction point |

|---|---|---|

| Hull war | Physical loss/damage from hostile acts | Transit declarations in listed areas |

| P&I war extension | Third-party liability linked to conflict events | Limit adequacy for major casualty scenarios |

| Cargo war | Cargo loss from war perils | Allocation between seller/buyer by contract |

| Ancillary security cover | Response costs, specialist support | Trigger wording and reimbursement evidence |

How are Strait of Hormuz premiums priced?

For most commercial voyages, war pricing is quoted as an additional premium (AP) for a specified voyage window, often expressed as a percentage of insured value. The base math is straightforward: insured value times quoted AP rate. The hard part is that the rate itself can reset quickly when threat tempo changes. Underwriters watch incident severity, weapon type, route concentration, intelligence from maritime advisories, and claim frequency. If those signals worsen, quotes can widen materially between fixtures only days apart.

The pricing engine also includes operational modifiers. Tankers carrying high-value cargo through a narrow lane face different expected loss profiles than container vessels with diversified cargo and different voyage tempo. Crew nationality, security protocols, timing of transit, and whether a vessel can avoid certain coordinates can all influence pricing. This is why "market average premium" headlines are often directionally right but operationally weak: two ships in the same week can receive very different terms.

The key public indicators for repricing are advisory channels and incident reporting cadence. The US MARAD maritime security advisories and UKMTO updates are watched across broker desks and risk committees because they anchor threat narrative with official operational guidance. When advisories become more frequent or specific, underwriters typically harden terms first through higher AP quotes, then through tighter conditions if volatility persists.

Illustrative premium mechanics

Assume a vessel insured at $100 million receives a 0.20% additional premium for listed-area transit. The incremental insurance line is $200,000 for that voyage period before brokerage and related costs. If risk perception doubles and the AP moves to 0.40%, that line becomes $400,000. Owners and charterers then decide whether to pass through, absorb, reroute, or delay. In energy lanes where timing and freight utilization are tight, most of that incremental cost moves downstream quickly.

That pass-through is why insurance can front-run commodity headlines. In our related oil shock explainer, physical supply risk is one part of the price response; insurance and freight repricing is another. Even if actual barrel flow continues, higher voyage economics can still lift delivered cost. The market is pricing expected disruption and risk transfer, not only realized closure.

Who pays the surcharge and how does it hit prices?

In freight practice, "who pays" is a contract question first and a market-power question second. Charter-party clauses can allow owners to recover additional war risk premiums directly, often via explicit war risk surcharge language. On liner trades, carriers may apply emergency risk surcharges or seasonal security adders when corridor risk rises. For crude and products, charter forms and recapture provisions determine how AP gets allocated between owner, charterer, and cargo interest.

The downstream effect is broad because shipping insurance lines rarely stay isolated. A higher AP can combine with longer routes, higher bunker burn, security measures, and schedule unreliability. The result is total delivered-cost inflation that appears in refinery margins, petrochemical input costs, and eventually consumer-facing energy or goods pricing. This linkage is one reason the site's market impact coverage and gas price analysis treat shipping insurance as a core transmission channel, not a footnote.

Financial risk managers also care about liquidity timing. Premiums and surcharges are cash outflows now; revenue recovery can lag by billing cycle or contract dispute. During fast escalation, working capital strain can rise even for operators that ultimately pass through costs. Smaller players with weaker credit lines can be forced into conservative routing choices earlier than large incumbents, which can further tighten capacity and push rates up for everyone else.

In escalation phases, insurance is often the first hard cost signal and the last cost line to fully normalize.

Contract levers that change outcome

Operators generally review five levers before committing voyages: war-clause wording, right to refuse unsafe ports or routes, notice period for surcharge pass-through, force majeure scope, and sanctions-compliance carve-outs. A strong clause set does not eliminate risk, but it prevents avoidable disputes after the voyage. Weak wording can leave parties arguing over liability while the next AP invoice is already due.

For cargo owners, the most practical move is pre-agreed surcharge governance. Define documentation standards, trigger thresholds, and dispute timelines before escalation events. That reduces invoice friction and allows risk teams to make faster routing decisions under pressure.

How operators reduce insurance exposure during escalation

Risk reduction is mostly operational discipline, not prediction. Teams that perform well in volatile windows run a repeatable playbook: route planning with defined fallback options, pre-approved declaration workflow, vessel-specific threat briefs, bridge-team drills, and synchronized communication between operations, legal, treasury, and brokers. The objective is to keep decision latency low when the market reprices overnight.

Operationally, firms usually separate actions into pre-fixture, pre-transit, and post-incident phases. Pre-fixture is contract hygiene and quote benchmarking. Pre-transit is declaration timing, route verification, and crew readiness. Post-incident is evidence capture, broker notification, and claim staging. The companies that skip phase discipline usually pay through higher AP, slower claims resolution, or preventable counterparty disputes.

Industry security baselines also matter. The International Maritime Organization security framework pages and regional best-practice guidance inform voyage risk controls that insurers monitor. Even when not explicitly mandatory, evidence of robust controls can support underwriting confidence and improve renewal conversations after a crisis cycle.

Five practical controls with high payoff

- Live advisory integration: wire MARAD and UKMTO updates into dispatch workflows rather than relying on ad hoc email checks.

- Voyage declaration calendar: treat notice windows as hard deadlines with internal accountability.

- Clause library: maintain pre-negotiated war-risk language for fast fixture cycles.

- Cost pass-through protocol: define surcharge invoicing evidence and approval chain before the first AP spike.

- Claims readiness package: preserve logs, notices, route traces, and communications from day one of escalation.

These controls do not guarantee low premiums. They do, however, prevent self-inflicted pricing penalties and reduce recovery lag when incidents occur.

What should readers monitor week to week?

For investors, importers, and policy teams, the most useful approach is a short signal dashboard. Watch advisory frequency, reported incident severity, vessel routing behavior, and explicit surcharge announcements by major carriers. When those four indicators move together, cost pressure is probably durable rather than temporary. If only one indicator moves, the market may be reacting to headline risk more than structural deterioration.

The site's existing Strait of Hormuz scenario page provides route context, while this page gives the insurance transmission layer. Together, they explain why oil and freight markets can react sharply even before physical closure events. For policy analysts, this distinction is important: insurance-driven cost shocks can arrive faster than diplomatic timelines and can persist after tactical de-escalation if underwriters continue to price residual uncertainty.

One final caution: do not confuse short-term quote relief with full normalization. Premiums often decline in steps, not all at once, because underwriters wait for sustained evidence that attack tempo and targeting intent have changed. Contract surcharges can also outlast quote improvements due to billing cycles and lagged negotiations. In practice, the path down is usually slower than the path up.

FAQ

What does war risk insurance shipping cover?

It generally covers conflict-linked perils excluded from standard marine terms, including hostile acts, mines, missile attacks, and detention tied to conflict conditions. Exact scope depends on policy wording, listed-area declarations, and endorsements. Operators should treat wording review as an operational step, not just a legal formality.

How are Strait of Hormuz war risk premiums calculated?

They are typically quoted as an additional percentage of insured value for a voyage or short period, then adjusted for threat signals, vessel type, route, and mitigation posture. Underwriters can reprice rapidly when incident data changes. That speed is why costs can jump between fixtures in the same week.

Who pays war risk surcharges in freight contracts?

Allocation follows charter-party and sales-contract language, but additional premiums are often passed through as explicit war risk or security surcharges. Where wording is ambiguous, disputes are common and cash recovery can lag. Pre-agreed surcharge governance lowers that friction.

Can vessels transit without war risk insurance?

Technically some firms could self-insure portions, but most lenders, counterparties, and internal risk committees require dedicated war cover for high-threat corridors. Sailing without it can create covenant, legal, and operational exposure. For most commercial operators, it is not a practical option.

How quickly do premiums fall after de-escalation?

Usually more slowly than they rise. Underwriters need sustained evidence of lower incident probability before normalizing terms, and contract surcharges may persist through billing cycles. Expect staged relief rather than instant reversion.

Sources

- US Energy Information Administration, Strait of Hormuz chokepoint data. eia.gov

- US Maritime Administration advisories and alerts. marad.dot.gov

- UK Maritime Trade Operations notices. ukmto.org

- International Maritime Organization security resources. imo.org

- Lloyd's market context for marine war-risk placement. lloyds.com